Housing Market Predictions for 2026: Will Home Prices Finally Drop?

The U.S. housing market continues its slow march toward balance as 2025 winds down. Buyers are gaining a little more breathing room thanks to moderating home prices, rising inventory, and slightly friendlier mortgage rates. Still, many remain cautious—waiting to see what 2026 will bring.

According to experts featured in the full report from Forbes Advisor, the big picture is clear: expect gradual price growth, relatively stable rates, and the most buyer-friendly conditions in markets with rising supply and strong local economies.

Fed Cuts Rates Again: Will Mortgage Rates Ease?

The Federal Reserve delivered its third rate cut of the year, dropping the benchmark rate to its lowest point since 2022. Mortgage rates, while not directly tied to the federal funds rate, tend to follow its overall trend.

Fed Chair Jerome Powell noted that inflation data remains limited but steady, keeping expectations for stable economic conditions heading into 2026.

The 2026 Housing Market Forecast

National home price growth slowed to just 1.3% annually in October 2025—one of the softest readings in years.

Regional highlights:

Miami, Tampa, and Phoenix: experiencing price declines

Chicago, Cleveland, NYC: showing modest gains

Most analysts expect 1% to 2% national growth in 2026—not a crash, but not a return to pandemic-era surges either.

Will the Housing Market Crash?

Short answer: Highly unlikely.

Inventory is still below pre-pandemic levels, and homeowners continue to hold strong equity positions. Even with cooling prices in some markets, there is no clear trigger for a widespread collapse.

“The record low supply of houses on the market protects against a market crash.” — Tom Hutchens, Angel Oak Mortgage Solutions

When Will the Market Fully Recover?

A meaningful recovery depends on two major shifts:

More homes hitting the market

Mortgage rates falling into the upper‑5% range

Both could happen in 2026—but the pace will vary regionally.

How Today’s Payments Compare to Last Year

The Forbes Advisor mortgage calculator shows a clear benefit to 2025 buyers. With rates lower than in 2024, a typical buyer saves $106 per month and over $38,000 in lifetime interest.

Existing & Pending Home Sales: What the Numbers Show

Existing-home sales ticked up 1.2% in October 2025, reaching 4.1 million transactions. Pending sales also climbed 1.9%, particularly in the Midwest and South where affordability remains stronger.

NAR’s Lawrence Yun notes that seasonal slowdowns may offer buyers more negotiating power during winter months.

Housing Inventory Outlook

Inventory is rising in several key markets, including Austin, San Antonio, and Tampa—areas that overheated during the pandemic. Meanwhile, markets like Buffalo, Cleveland, and Pittsburgh continue facing tight supply.

If mortgage rates drop significantly, expect inventory to tighten again as demand surges.

Should You Wait to Buy?

“The best time for buyers is when they find a home they like, can afford, and fits their family’s needs.” — Orphe Divounguy, Zillow Home Loans

Trying to perfectly time the market rarely works. Rising prices, shifting inventory, and uncertain rates make preparation more important than prediction.

Pro Tip: If you’re building a long‑term real estate career, staying informed is just as important as staying licensed.

Real estate professionals in Florida and beyond trust Cameron Academy for licensing, continuing education, and professional development.

Pro Tips for Buyers

Know your true budget—monthly payments matter more than listing prices.

Be flexible with size, features, and location.

Study local inventory trends and days on market.

Stay patient and avoid stretching beyond your means.

Pro Tips for Sellers

Research comparable properties and price competitively.

Ensure the home looks its best—online curb appeal matters.

Work with a knowledgeable local agent.

Fix known issues before listing to avoid buyer objections.

FAQs

Will lower mortgage rates push prices up?

Yes. Lower rates increase demand, which pressures prices upward—especially in tight markets.

What happens if the market crashes?

Home values fall, foreclosures rise, and inventory balloons. However, experts agree a 2026 crash is highly unlikely.

Is it smart to buy real estate before a recession?

For long-term homeowners: usually yes. For short-term investors: more risky.

Final Thoughts

The 2026 housing market won’t look like the frenzy of 2021 nor the tight freeze of 2023–2024. Instead, buyers and sellers should expect a slow return toward balance—with opportunities strongest in markets gaining inventory.

And if you’re working toward becoming a real estate professional—or expanding your credentials—now is an excellent time to strengthen your expertise. Visit Cameron Academy for real estate, mortgage, insurance, and professional licensing across the nation.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

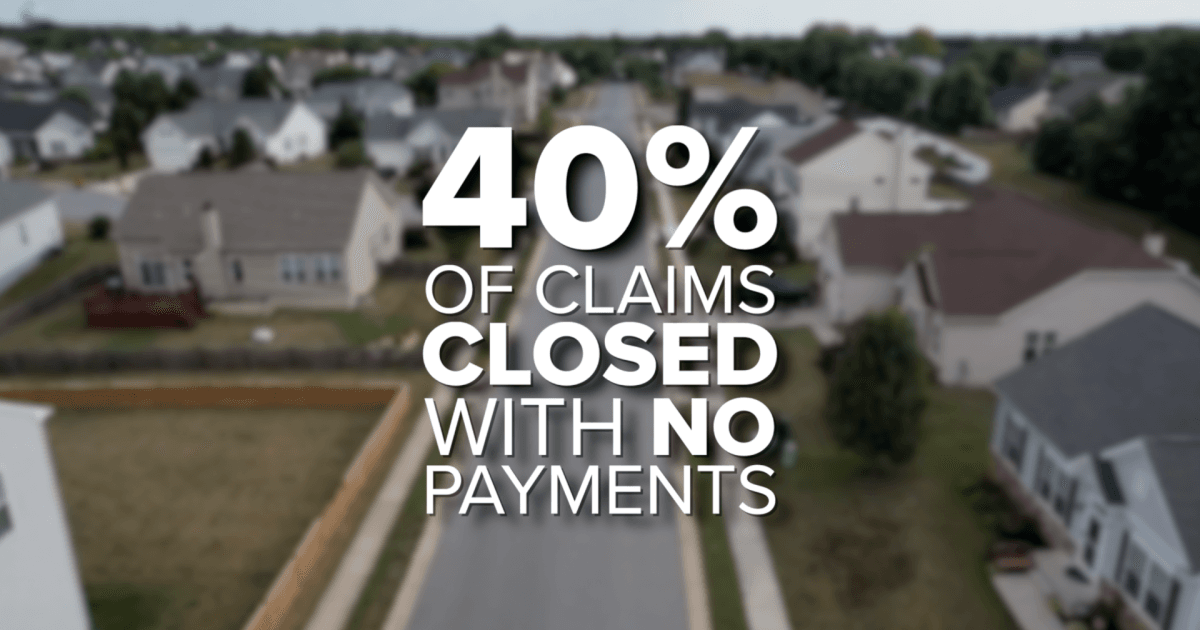

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}