In the world of commercial real estate, optimism is cautiously building as we move further into 2025. The market correction that began in mid-2022 is showing signs of recovery, with interest rates declining and transactional activity stabilizing. This nascent recovery is not uniform, however, and varies across different segments of the market.

The recent downturn was driven by familiar cyclical factors such as rising rates and a reversal in overheated yield compression, compounded by structural changes like the shift in office use. As the market begins to recover, the pace will differ across sectors, presenting both opportunities and risks for investors.

Investors are increasingly focusing on emerging property types, driven by technological and demographic shifts, while others see value in traditional sectors at cyclical lows. The combination of debt-refinancing stress and the structural challenges of commodity-office assets is expected to continue influencing price discovery.

Active management and asset selection are becoming crucial as yield compression no longer provides a tailwind for returns. Understanding the key factors driving performance through attribution analysis will be vital in this environment.

Despite market-based risks, geopolitical and economic uncertainties persist, and climate risk remains a significant concern. The global economy’s drift away from net-zero targets raises fears of more frequent and severe climate-induced weather events, as highlighted by the multiple extreme-weather disasters of 2024.

Recovery — Not Everywhere All at Once

Two years after the slowdown began, the global property market is entering a recovery phase. Transaction volumes and values have bottomed out, and interest rates have peaked. In 2025, lower interest rates are expected to facilitate closer pricing alignment between buyers and sellers, improving liquidity.

Investor preferences are shifting towards the living sector, industrial assets, and properties exposed to broader socioeconomic and technological changes. A notable transaction in 2024 was Blackstone Inc.’s $16 billion acquisition of data-center operator AirTrunk, underscoring the demand for data centers and new energy infrastructure.

Fundraising for property investment remains challenging, with low deal activity stalling distributions from closed-end funds. The emergence of private credit and the outperformance of debt versus equity funds have made debt a preferred route for many investors.

While the market has not experienced a major distress cycle like that of the 2008 financial crisis, distress levels are rising. This may aid recovery by providing opportunities for well-capitalized players to acquire assets at a discount.

Office and retail properties have suffered significant value destruction, deterring many investors. However, some players are returning, drawn by pockets of outperformance. Despite this, it is unlikely that aggregate deal volumes for these property types will return to long-term averages soon.

Investment Pendulum Swings Back to Asset Selection

As we enter a new investment cycle, the focus is increasingly on active asset selection and management. With evolving market conditions, the playbook for delivering returns is changing.

Selecting the right assets has always been crucial in commercial real estate. Unlike public equities, investors cannot simply buy the market. They must balance top-down allocation strategies with granular, bottom-up asset-selection and management decisions.

Attribution analysis can provide insights into the evolving nature of performance drivers. Evidence from the MSCI/PREA U.S. ACOE Quarterly Property Fund Index highlights this variability. Historically, selection accounted for around 63% of deviation from the benchmark among funds, but the influence of allocation and selection has shifted over time.

Underwater Assets Come to Light

Ongoing price declines and higher interest rates have cast doubt on some borrowers’ ability to repay or refinance commercial-property loans. In Europe, substantial corrections since mid-2022 have left many properties worth less than their acquisition prices, particularly those bought near the market’s peak in 2021.

In the U.S., an estimated $500 billion of loans are set to mature in 2025. If these loans were to mature at Q3 2024 price levels, approximately 14% would be underwater, with asset values below outstanding loan balances.

U.S. offices face the bleakest refinancing prospects in 2025, with nearly 30% of maturing office loans associated with properties estimated to be worth less than the secured debt. The apartment market also faces challenges, with $19 billion worth of properties below loan values.

Investors Get to Grips with Physical Climate Risk

Extreme weather events are expected to become more common, potentially impacting real-estate values through higher insurance premiums and repair costs. The relationship between transaction yields and physical climate risk is being scrutinized, with higher-risk assets currently trading at a premium.

As climate risks intensify, pricing should adjust to reflect the increased threat to property values from extreme weather exposure. Investors can get a head start by considering climate-related risks in their portfolios.

Property Investors Seek a Ride on the AI Train

The rapid development of AI is driving demand for data centers. Blackstone’s acquisition of AirTrunk and other major investments highlight this trend. Data centers are seeing increased interest from generalist property investors, leading to a more diverse range of deal structures.

While the data-center market presents opportunities, it also carries unique risks. Operating a data center requires specific expertise, and data transparency is lower than for traditional property types. Investors with experience in the sector have a significant informational advantage.

For more detailed insights, you can refer to the original article on MSCI’s website.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

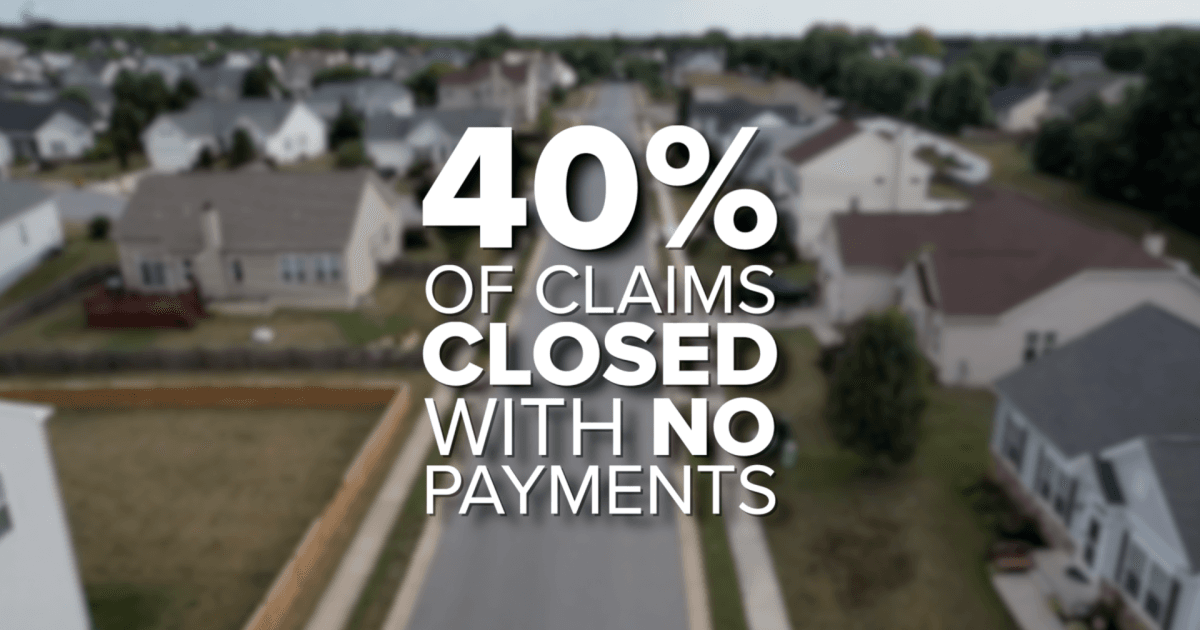

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}