In the world of commercial real estate, optimism is cautiously building as we move further into 2025. The market correction that began in mid-2022 is showing signs of recovery, with interest rates declining and transactional activity stabilizing. This nascent recovery is not uniform, however, and varies across different segments of the market.

The recent downturn was driven by familiar cyclical factors such as rising rates and a reversal in overheated yield compression, compounded by structural changes like the shift in office use. As the market begins to recover, the pace will differ across sectors, presenting both opportunities and risks for investors.

Investors are increasingly focusing on emerging property types, driven by technological and demographic shifts, while others see value in traditional sectors at cyclical lows. The combination of debt-refinancing stress and the structural challenges of commodity-office assets is expected to continue influencing price discovery.

Active management and asset selection are becoming crucial as yield compression no longer provides a tailwind for returns. Understanding the key factors driving performance through attribution analysis will be vital in this environment.

Despite market-based risks, geopolitical and economic uncertainties persist, and climate risk remains a significant concern. The global economy’s drift away from net-zero targets raises fears of more frequent and severe climate-induced weather events, as highlighted by the multiple extreme-weather disasters of 2024.

Recovery — Not Everywhere All at Once

Two years after the slowdown began, the global property market is entering a recovery phase. Transaction volumes and values have bottomed out, and interest rates have peaked. In 2025, lower interest rates are expected to facilitate closer pricing alignment between buyers and sellers, improving liquidity.

Investor preferences are shifting towards the living sector, industrial assets, and properties exposed to broader socioeconomic and technological changes. A notable transaction in 2024 was Blackstone Inc.’s $16 billion acquisition of data-center operator AirTrunk, underscoring the demand for data centers and new energy infrastructure.

Fundraising for property investment remains challenging, with low deal activity stalling distributions from closed-end funds. The emergence of private credit and the outperformance of debt versus equity funds have made debt a preferred route for many investors.

While the market has not experienced a major distress cycle like that of the 2008 financial crisis, distress levels are rising. This may aid recovery by providing opportunities for well-capitalized players to acquire assets at a discount.

Office and retail properties have suffered significant value destruction, deterring many investors. However, some players are returning, drawn by pockets of outperformance. Despite this, it is unlikely that aggregate deal volumes for these property types will return to long-term averages soon.

Investment Pendulum Swings Back to Asset Selection

As we enter a new investment cycle, the focus is increasingly on active asset selection and management. With evolving market conditions, the playbook for delivering returns is changing.

Selecting the right assets has always been crucial in commercial real estate. Unlike public equities, investors cannot simply buy the market. They must balance top-down allocation strategies with granular, bottom-up asset-selection and management decisions.

Attribution analysis can provide insights into the evolving nature of performance drivers. Evidence from the MSCI/PREA U.S. ACOE Quarterly Property Fund Index highlights this variability. Historically, selection accounted for around 63% of deviation from the benchmark among funds, but the influence of allocation and selection has shifted over time.

Underwater Assets Come to Light

Ongoing price declines and higher interest rates have cast doubt on some borrowers’ ability to repay or refinance commercial-property loans. In Europe, substantial corrections since mid-2022 have left many properties worth less than their acquisition prices, particularly those bought near the market’s peak in 2021.

In the U.S., an estimated $500 billion of loans are set to mature in 2025. If these loans were to mature at Q3 2024 price levels, approximately 14% would be underwater, with asset values below outstanding loan balances.

U.S. offices face the bleakest refinancing prospects in 2025, with nearly 30% of maturing office loans associated with properties estimated to be worth less than the secured debt. The apartment market also faces challenges, with $19 billion worth of properties below loan values.

Investors Get to Grips with Physical Climate Risk

Extreme weather events are expected to become more common, potentially impacting real-estate values through higher insurance premiums and repair costs. The relationship between transaction yields and physical climate risk is being scrutinized, with higher-risk assets currently trading at a premium.

As climate risks intensify, pricing should adjust to reflect the increased threat to property values from extreme weather exposure. Investors can get a head start by considering climate-related risks in their portfolios.

Property Investors Seek a Ride on the AI Train

The rapid development of AI is driving demand for data centers. Blackstone’s acquisition of AirTrunk and other major investments highlight this trend. Data centers are seeing increased interest from generalist property investors, leading to a more diverse range of deal structures.

While the data-center market presents opportunities, it also carries unique risks. Operating a data center requires specific expertise, and data transparency is lower than for traditional property types. Investors with experience in the sector have a significant informational advantage.

For more detailed insights, you can refer to the original article on MSCI’s website.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

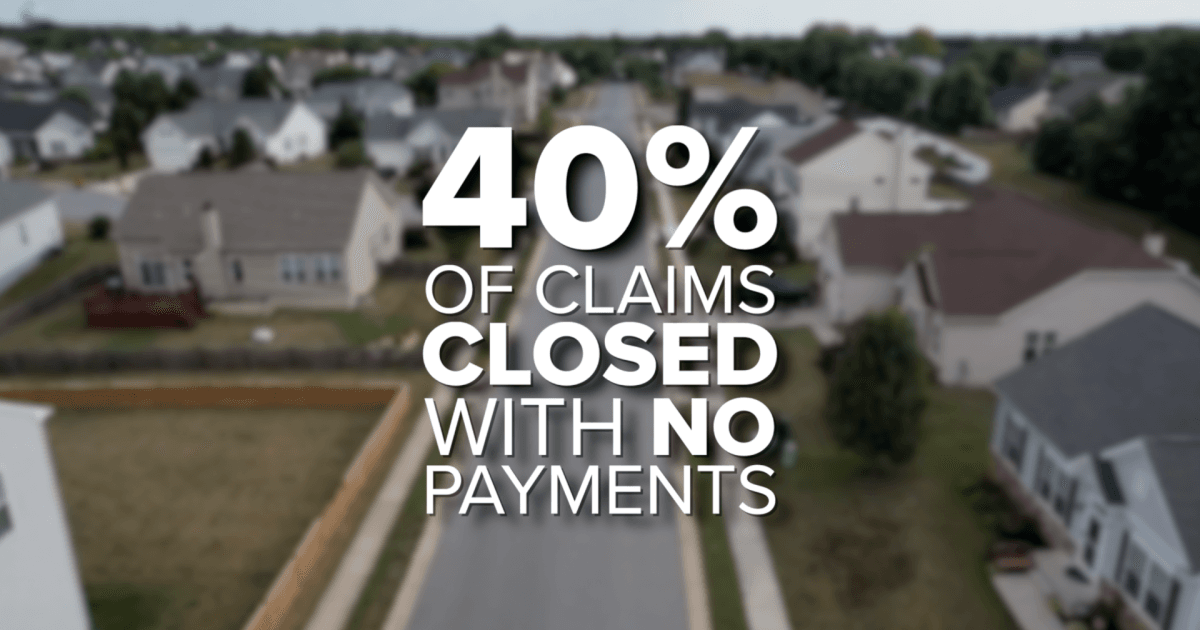

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}