Rising Home Insurance Costs Are Quietly Reshaping America’s Real Estate Market

Across the United States, a new force is beginning to reshape local real estate markets — and it isn’t mortgage rates, inflation, or even inventory shortages. It’s home insurance. In the most disaster‑prone areas, skyrocketing premiums are eating directly into home values, upending long‑held assumptions about affordability, risk, and long‑term investment viability.

The New York Times recently published a deeply reported investigation into this rapidly expanding crisis, revealing how rising premiums — often fueled by global reinsurance upheavals — are placing thousands of homeowners under intense financial pressure. Their reporting, grounded in national data and real‑world interviews, highlights an emerging trend that real estate professionals must watch closely.

When Insurance Becomes the Dealbreaker

In coastal Louisiana, residents are facing insurance increases that would have seemed unimaginable just a few years ago. Sandra Rojas, a fifth‑generation resident of Lafitte, saw her annual premium soar to $8,312 — more than double what she paid four years earlier. She considered selling, but with home values in her region down 38% since 2020, her options are limited. “You’re kind of stuck where you are,” she said.

Similar stories are emerging nationwide. In Colorado, buyers are walking away from deals after failing to secure affordable wildfire coverage. In California, 13% of real estate agents report transactions falling apart because buyers couldn’t obtain insurance at all.

New research from the National Bureau of Economic Research provides numbers to match the stories. Disaster‑exposed ZIP codes are seeing home values fall in direct response to rising insurance costs. According to researchers Benjamin Keys and Philip Mulder, homes in the top 10% most exposed areas are selling for an average of $43,900 less than they would have otherwise.

Their study of 74 million payment records from 2014–2024 found that nearly one‑fifth of the national increase in premiums since 2017 is tied to “rapid repricing” of climate‑driven risks. Meanwhile, global reinsurers — absorbing mounting losses — have doubled the rates they charge insurers, who then pass the burden directly to homeowners.

A Growing National Ripple Effect

In hail‑risk Midwest states, insurance now consumes more than 20% of total housing payments. In parts of Louisiana, it exceeds 30%. For buyers, this means steeper monthly costs. For sellers, it means fewer qualified buyers and declining property values.

Some homeowners are even dropping coverage entirely. In Lafitte, Clarence Guidry received a quote for a $20,000 premium — plus a $50,000 hurricane deductible. Unable to sustain the cost, he paid off his mortgage and now self‑insures. He’s not alone: 13% of U.S. homeowners are now uninsured.

What This Means for Real Estate and Professional Licensees

Insurance‑driven pricing pressures are no longer hypothetical — they are here, reshaping how agents, lenders, appraisers, and insurance professionals work. Deals stall, lenders tighten, buyers hesitate, and municipalities face shrinking tax revenue as home values cool.

For professionals, especially those working in high‑risk states like Florida, staying current on these shifts is essential. Cameron Academy offers real‑estate and insurance licensing education designed to help professionals understand not only the rules of their industry but also the evolving economic forces that shape it. Understanding how climate‑risk and insurance impacts property value is now a core professional skill.

Looking Forward

As reinsurers adjust their risk models and climate‑driven disasters grow more severe, insurance premiums are projected to keep rising. Industry analysts expect home values in high‑risk markets to adjust further downward as buyers push for affordability.

For many Americans, the dilemma is becoming painfully clear: pay soaring premiums, sell at a loss, or self‑insure and hope for the best.

Real estate, insurance, lending, and financial professionals will need to stay educated and adaptable — and up‑to‑date training is one of the most powerful tools available.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

In 2026, financial advisors are no longer just experimenting with AI — they’re relying on it. Once confined to back-office duties, AI now supports meeting prep, portfolio analysis, and even early-stage financial planning. Advisors say the tech is strengthening client relationships by freeing them from administrative overload, though entry-level roles like paraplanners may feel the squeeze as automation accelerates.

Cybercriminals are weaponizing AI to launch highly convincing email scams and system breaches across the mortgage industry, overwhelming lenders and servicers whose cybersecurity measures can’t keep up. With major companies already hit and regulation lagging behind, experts warn the sector—now considered critical infrastructure—must rapidly upgrade protections, collaborate on threat intelligence, and improve AI governance before the risks escalate further.

Escrow payments are quietly surging across the country as property taxes and insurance premiums spike—pushing many homeowners toward delinquencies and even foreclosure. New data from Cotality shows the sharpest increases hitting the South and Midwest, with Florida among the hardest‑hit states. Even with fixed mortgage rates, rising escrow requirements are driving monthly payments higher and threatening affordability heading into 2026.

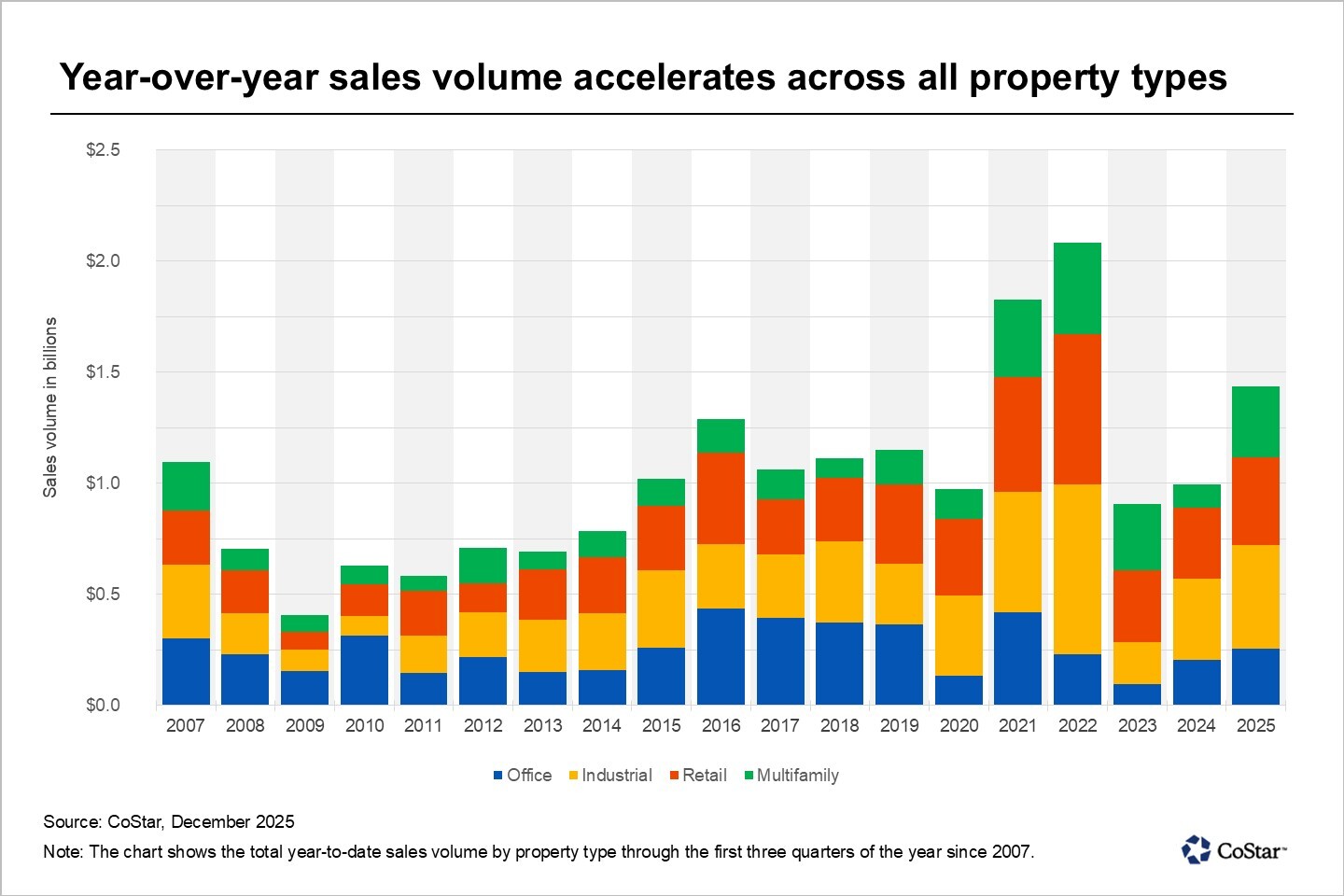

Milwaukee entered 2025 with renewed momentum, posting its strongest commercial real estate sales volume in three years. After a period of uncertainty and high capital costs, investors are returning with a sharper focus on quality assets, realistic pricing, and reliable cash flow. Activity is increasing across industrial, office, multifamily, and retail sectors, signaling a broad-based recovery fueled by stabilizing interest rates and improved market confidence.

As 2026 approaches, the title insurance industry is navigating a complex mix of market recovery, rising fraud threats, and sweeping regulatory changes. Industry leaders say the path forward centers on smarter technology, leaner operations, and stronger support for title agents. With AI-driven workflows, enhanced fraud prevention, and new compliance demands—including FinCEN’s expanded Geographic Targeting Orders—companies like Stewart and First American are reshaping how title work gets done. For real estate and mortgage professionals, the year ahead promises more automation, heightened standards, and major opportunities for those who stay ahead of the curve.

The real estate industry is undergoing a major transformation in 2025 as advancements in AI, proptech, blockchain, and data intelligence redefine how properties are marketed, valued, financed, and experienced. From instant digital valuations and immersive virtual tours to tokenized investments and predictive analytics, technology is reshaping every stage of the real estate lifecycle. Professionals who embrace these innovations—while maintaining the human expertise clients still rely on—will lead the next era of the industry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}