On June 24, 2024, a significant development unfolded in the real estate industry as six federal agencies finalized a rule to implement safeguards for Automated Valuation Models (AVMs). This rule, established by the Department of the Treasury, Federal Reserve System, Federal Deposit Insurance Corporation, National Credit Union Administration, Consumer Protection Financial Bureau, and Federal Housing Finance Agency, aims to address the burgeoning use of AI-driven AVMs in property valuations.

AVMs have become indispensable tools in real estate, offering efficiency and speed in estimating property values for mortgage and lending services. However, the increasing reliance on these AI-powered models has raised concerns about data accuracy, security, and potential discriminatory impacts. The newly finalized rule mandates the integration of five quality control measures to mitigate these concerns.

The Rule’s Key Provisions

The rule requires companies utilizing AVMs to ensure:

A high level of confidence in valuation estimates.

Protection against data manipulation.

Avoidance of conflicts of interest.

Random sample testing and reviews.

Compliance with applicable nondiscrimination laws.

This regulatory framework is designed to ensure that AVMs provide accurate and equitable property valuations, aligning with the principles of the Fair Housing Act, which prohibits discrimination in housing-related activities.

Historical Context and Impact

The adoption of AVMs has accelerated due to advancements in AI and the shortage of human appraisers exacerbated by the COVID-19 pandemic. A report by the Brookings Institution highlights the critical role these models play for organizations like Fannie Mae and Freddie Mac. Despite their benefits, AVMs have faced scrutiny for potentially perpetuating biases present in human-performed appraisals.

The finalized rule follows a proposed rule issued on June 1, 2023, in response to the Dodd-Frank Act. This proposal laid the groundwork for quality control standards, echoing the Biden administration’s executive orders on minimizing bias in AI processes.

Looking Ahead

When the rule takes effect a year after its publication in the Federal Register, it will represent a pivotal step in enhancing the integrity of real estate valuations. Companies are granted the flexibility to develop specific policies that align with their size and risk profile, ensuring a dynamic regulatory environment that evolves with technological advancements.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

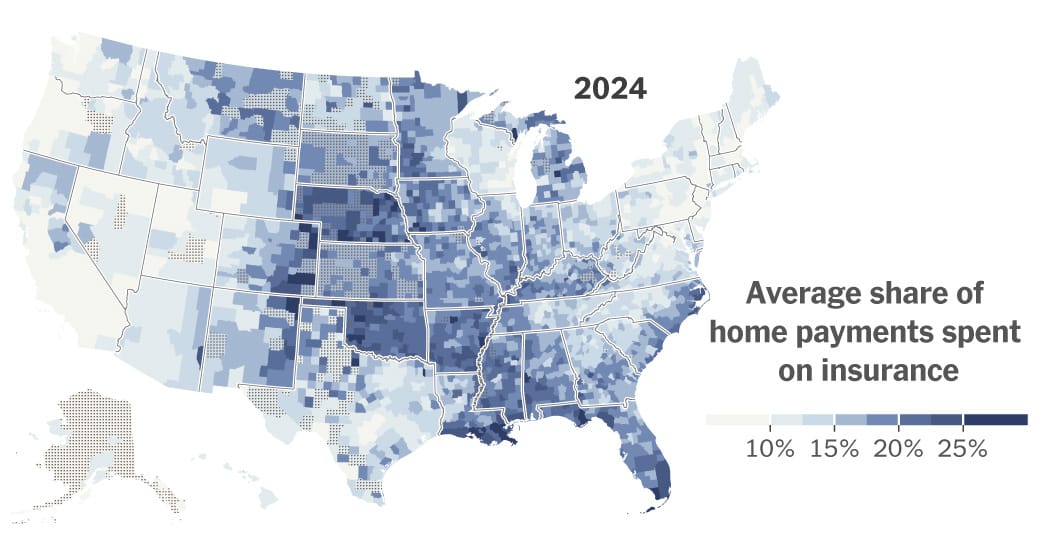

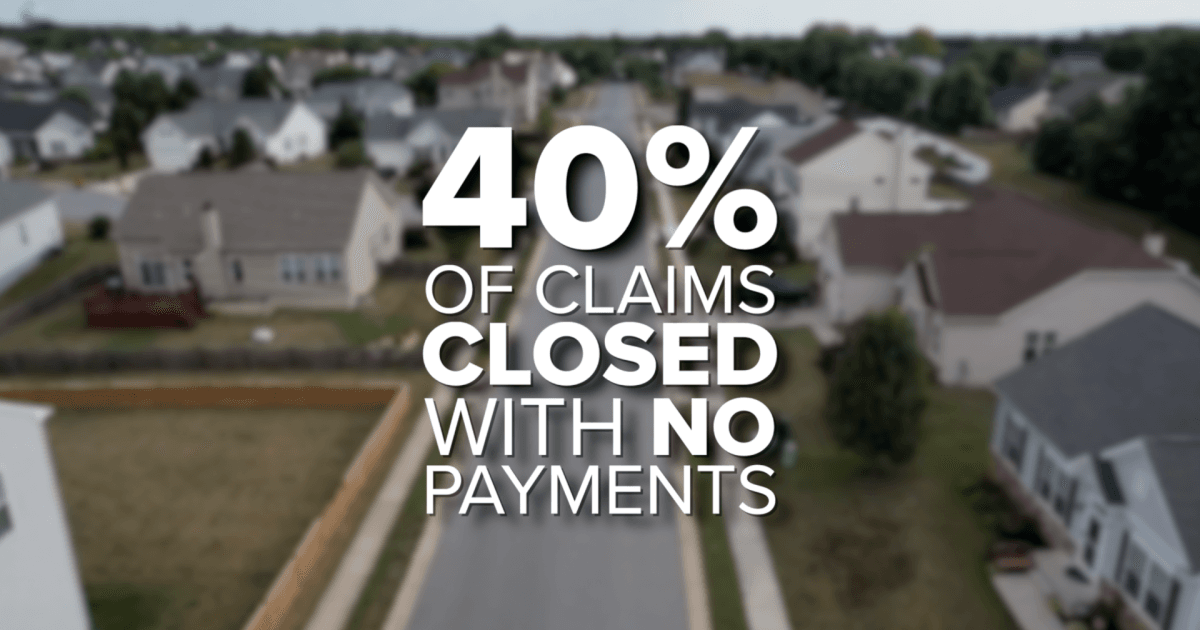

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}