On June 24, 2024, a significant development unfolded in the real estate industry as six federal agencies finalized a rule to implement safeguards for Automated Valuation Models (AVMs). This rule, established by the Department of the Treasury, Federal Reserve System, Federal Deposit Insurance Corporation, National Credit Union Administration, Consumer Protection Financial Bureau, and Federal Housing Finance Agency, aims to address the burgeoning use of AI-driven AVMs in property valuations.

AVMs have become indispensable tools in real estate, offering efficiency and speed in estimating property values for mortgage and lending services. However, the increasing reliance on these AI-powered models has raised concerns about data accuracy, security, and potential discriminatory impacts. The newly finalized rule mandates the integration of five quality control measures to mitigate these concerns.

The Rule’s Key Provisions

The rule requires companies utilizing AVMs to ensure:

A high level of confidence in valuation estimates.

Protection against data manipulation.

Avoidance of conflicts of interest.

Random sample testing and reviews.

Compliance with applicable nondiscrimination laws.

This regulatory framework is designed to ensure that AVMs provide accurate and equitable property valuations, aligning with the principles of the Fair Housing Act, which prohibits discrimination in housing-related activities.

Historical Context and Impact

The adoption of AVMs has accelerated due to advancements in AI and the shortage of human appraisers exacerbated by the COVID-19 pandemic. A report by the Brookings Institution highlights the critical role these models play for organizations like Fannie Mae and Freddie Mac. Despite their benefits, AVMs have faced scrutiny for potentially perpetuating biases present in human-performed appraisals.

The finalized rule follows a proposed rule issued on June 1, 2023, in response to the Dodd-Frank Act. This proposal laid the groundwork for quality control standards, echoing the Biden administration’s executive orders on minimizing bias in AI processes.

Looking Ahead

When the rule takes effect a year after its publication in the Federal Register, it will represent a pivotal step in enhancing the integrity of real estate valuations. Companies are granted the flexibility to develop specific policies that align with their size and risk profile, ensuring a dynamic regulatory environment that evolves with technological advancements.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

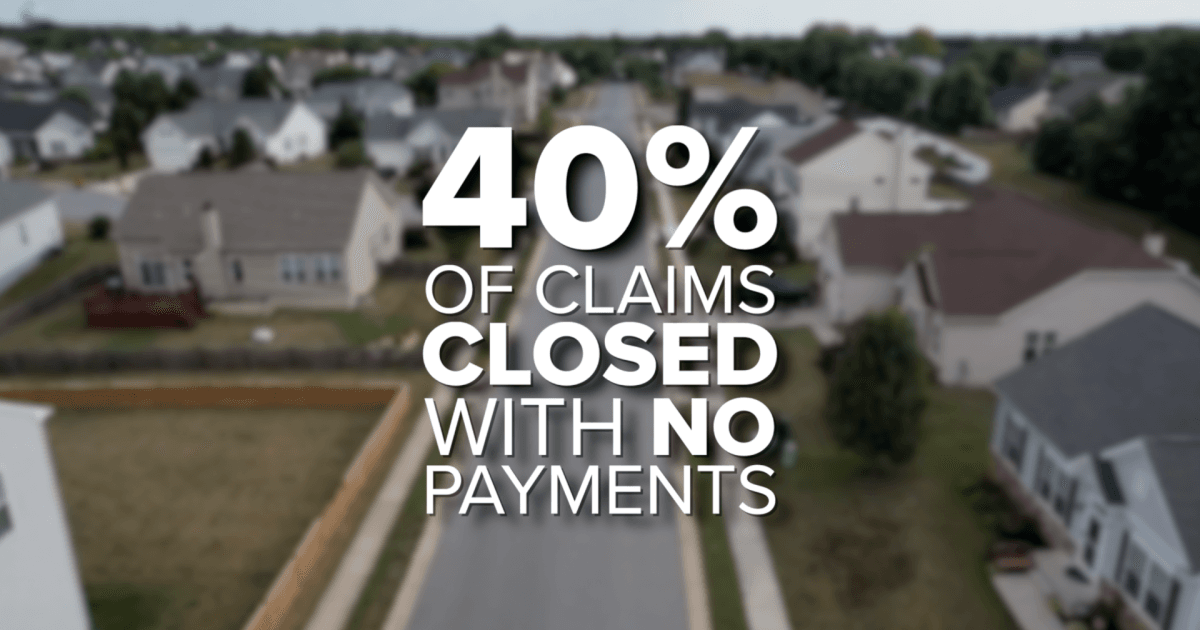

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}