In the ever-evolving landscape of real estate, the national housing market has reached a staggering valuation of $47.5 trillion, marking a $2.4 trillion increase over the past year. This remarkable growth, as highlighted in a preliminary Redfin analysis, underscores the profound impact of remote work on housing trends.

Remote Work and Secondary Cities

A key driver of this surge is the allure of remote work, which has reshaped the demand for housing in specific metropolitan areas. More affordable cities, often referred to as “secondary cities,” have emerged as significant beneficiaries. For instance, Newark, New Jersey, and New Haven, Connecticut, experienced notable increases in home values, with Newark’s housing market skyrocketing by 12.8% over the last year. This trend is largely due to their proximity to larger urban centers and their appeal to those priced out of expensive metros like New York.

The Subcity Phenomenon

The concept of a “subcity,” as described in a colloquial definition, plays a crucial role in this dynamic. These are cities that function as secondary hubs to larger metropolitan areas. With the remote work trend solidifying into a hybrid model, these subcities have become attractive alternatives, offering affordability and accessibility.

Winners and Losers in the Housing Market

While secondary cities flourish, traditional boomtowns and high-cost areas have faced stagnation or decline. Cities like Boise, Idaho, and New York City saw declines in home values, attributed to their already high prices or pandemic-fueled influxes that have since waned. Meanwhile, suburban and rural areas have also seen growth, with suburban home values rising by 5.6% to about $29 trillion.

Challenges for Prospective Buyers

Despite the overall market growth, prospective buyers face significant challenges. Elevated mortgage rates, limited inventory, and high home prices have made homeownership increasingly unaffordable. As reported by Fortune, the housing market experienced a freeze, with existing home sales plummeting to their lowest point in nearly three decades.

However, there is a silver lining. Experts anticipate that mortgage rates may start to decline before the end of 2024, potentially easing affordability concerns. Until then, homeowners continue to hold substantial housing wealth, benefiting from the supply shortage that maintains elevated home values.

Conclusion

As the housing market continues to evolve, the interplay between remote work, secondary cities, and economic factors will remain pivotal. For a deeper dive into these trends, you can explore the original article on Fortune’s website.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

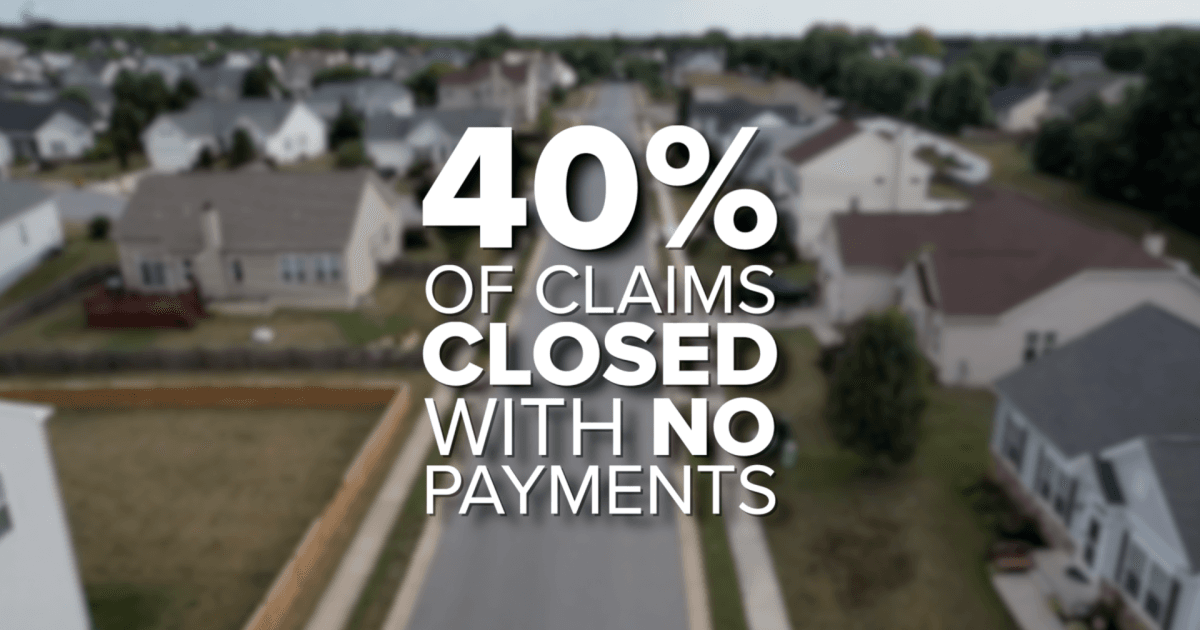

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}