In the ever-evolving landscape of real estate, the national housing market has reached a staggering valuation of $47.5 trillion, marking a $2.4 trillion increase over the past year. This remarkable growth, as highlighted in a preliminary Redfin analysis, underscores the profound impact of remote work on housing trends.

Remote Work and Secondary Cities

A key driver of this surge is the allure of remote work, which has reshaped the demand for housing in specific metropolitan areas. More affordable cities, often referred to as “secondary cities,” have emerged as significant beneficiaries. For instance, Newark, New Jersey, and New Haven, Connecticut, experienced notable increases in home values, with Newark’s housing market skyrocketing by 12.8% over the last year. This trend is largely due to their proximity to larger urban centers and their appeal to those priced out of expensive metros like New York.

The Subcity Phenomenon

The concept of a “subcity,” as described in a colloquial definition, plays a crucial role in this dynamic. These are cities that function as secondary hubs to larger metropolitan areas. With the remote work trend solidifying into a hybrid model, these subcities have become attractive alternatives, offering affordability and accessibility.

Winners and Losers in the Housing Market

While secondary cities flourish, traditional boomtowns and high-cost areas have faced stagnation or decline. Cities like Boise, Idaho, and New York City saw declines in home values, attributed to their already high prices or pandemic-fueled influxes that have since waned. Meanwhile, suburban and rural areas have also seen growth, with suburban home values rising by 5.6% to about $29 trillion.

Challenges for Prospective Buyers

Despite the overall market growth, prospective buyers face significant challenges. Elevated mortgage rates, limited inventory, and high home prices have made homeownership increasingly unaffordable. As reported by Fortune, the housing market experienced a freeze, with existing home sales plummeting to their lowest point in nearly three decades.

However, there is a silver lining. Experts anticipate that mortgage rates may start to decline before the end of 2024, potentially easing affordability concerns. Until then, homeowners continue to hold substantial housing wealth, benefiting from the supply shortage that maintains elevated home values.

Conclusion

As the housing market continues to evolve, the interplay between remote work, secondary cities, and economic factors will remain pivotal. For a deeper dive into these trends, you can explore the original article on Fortune’s website.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

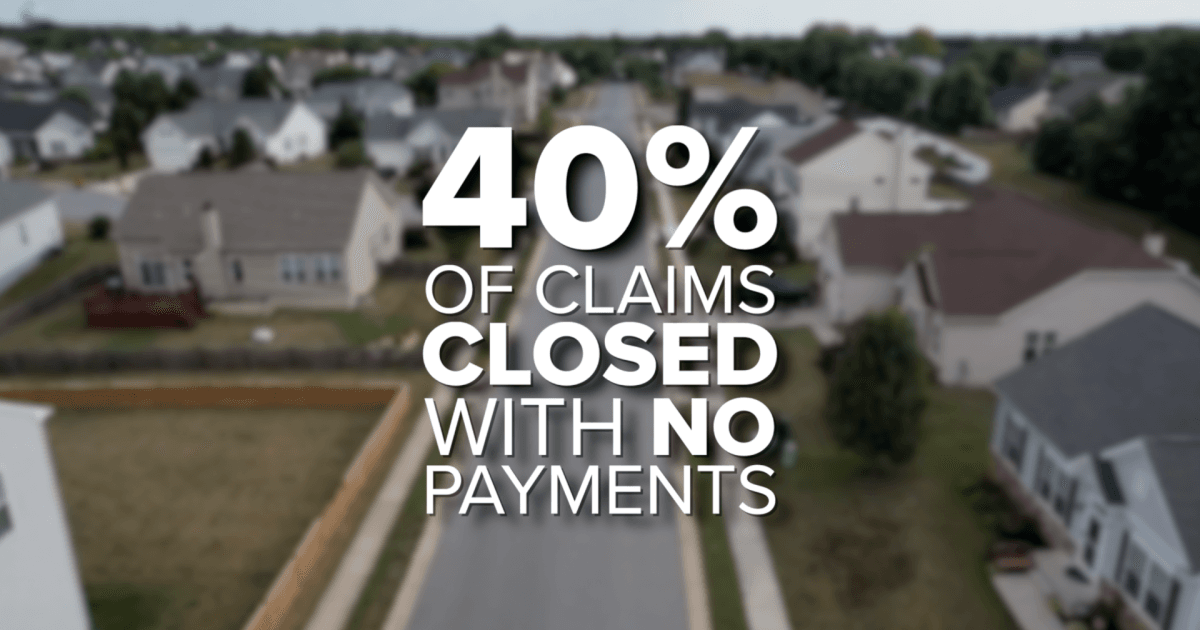

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}