Florida homeowners have been waiting years for relief from rising property insurance costs — and at long last, rate reductions are finally appearing. After a turbulent 2017–2024 era filled with hurricanes, legal chaos, and skyrocketing claim costs, legislative reforms passed in 2022 and 2023 have helped stabilize the market. Yet many homeowners are stunned to find their latest bill is still higher. If rates are down, why aren’t premiums following?

A recent Sun Sentinel opinion column by John W. Rollins, CEO of Patriot Select Property & Casualty Insurance Company, explains the hidden math behind this contradiction — and reveals what homeowners can actually do about it.

The Real Reason Premiums Keep Rising

Insurance premiums rely on two components: the rate (cost per $1,000 of replacement value) and the replacement value of the home. While rates soared during the height of Florida’s litigation surge, inflation simultaneously drove construction costs to record highs. Even now, as rates begin to fall, the replacement value continues to climb — and that value is what drives most of the final bill.

Florida’s Office of Insurance Regulation shows that the average premium per $1,000 of value rose from $4.59 in mid‑2022 to $5.15 in 2024, before easing to $5.00 in late 2025 — only a 9% increase over three years. Yet average total premiums jumped a staggering 34%, from $2,798 to $3,748.

Quick Insight: Nearly 75% of premium increases come from rising replacement values, not higher insurance rates.

So What Can Homeowners Do?

The good news? Homeowners have more control — and more options — than they might think.

1. Shop Around — Competition Is Back

Seventeen new insurers have joined Florida’s market since 2023, giving agents fresh options and homeowners renewed negotiating power. Falling rates mean potential savings for identical coverage.

2. Recalculate Your Replacement Value

Most companies rely on automated “inflation guard” adjustments, which may overshoot reality. Requesting a fresh valuation at renewal could prevent an unnecessary premium spike.

3. Reevaluate Your Risk

Improvements like updated roofs, new plumbing, hurricane‑resistant windows, or even a stronger credit score can meaningfully lower premiums. Discounts for seniors, veterans, smart home devices, and secure communities often go unused simply because insurers aren’t informed.

4. Consider Sharing More Risk

Choosing higher deductibles or opting for an “actual cash value” roof policy can reduce premiums significantly — just weigh the tradeoffs carefully after a claim.

A Turning Point for Florida

The broader industry outlook is increasingly optimistic. Reinsurance costs are falling. Litigation and fraudulent claims have plummeted. Market conditions are stabilizing. And for the first time in years, insurers are returning to Florida with confidence.

For real estate, mortgage, and insurance professionals, understanding these shifts is essential. At Cameron Academy, we help both new and seasoned professionals stay ahead of market changes that influence Florida’s property landscape. Whether you’re earning a real estate license, expanding into insurance, or deepening your industry expertise, staying educated gives you a major advantage in a transforming marketplace.

To dive deeper into Florida’s insurance data and analysis, read the full opinion piece by John W. Rollins at the Sun Sentinel website.

More Articles

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

After nearly 20 years under uniquely harsh lending rules, Florida may finally see its condo market freed from a 25% down payment requirement imposed only on the state. Industry leaders say Fannie Mae could announce changes as early as December—potentially restoring the standard 10% down payment used everywhere else in the country. Experts believe the shift would boost maintenance funding, improve affordability, and stabilize Florida’s condo market after years of strain.

Phoenix’s commercial real estate market is shaking off years of uncertainty as broker optimism hits its highest level since interest rates began climbing. The latest ASU Commercial Broker Sentiment Index soared to 62.7, signaling strong confidence across multifamily, retail, office, and capital markets. With population growth accelerating, interest rates easing, and AI boosting industry efficiency, Phoenix is positioning itself for a powerful run into 2026—offering meaningful opportunities for both new and seasoned real estate professionals.

Michigan’s House Rules Committee heard testimony on a proposal that would let licensed professionals complete all required continuing education online. Supporters say the change would modernize outdated rules, reduce costs, and improve access for rural and busy workers. The state licensing department backs the measure, and lawmakers noted it could reshape CE options across industries from real estate to insurance and healthcare.

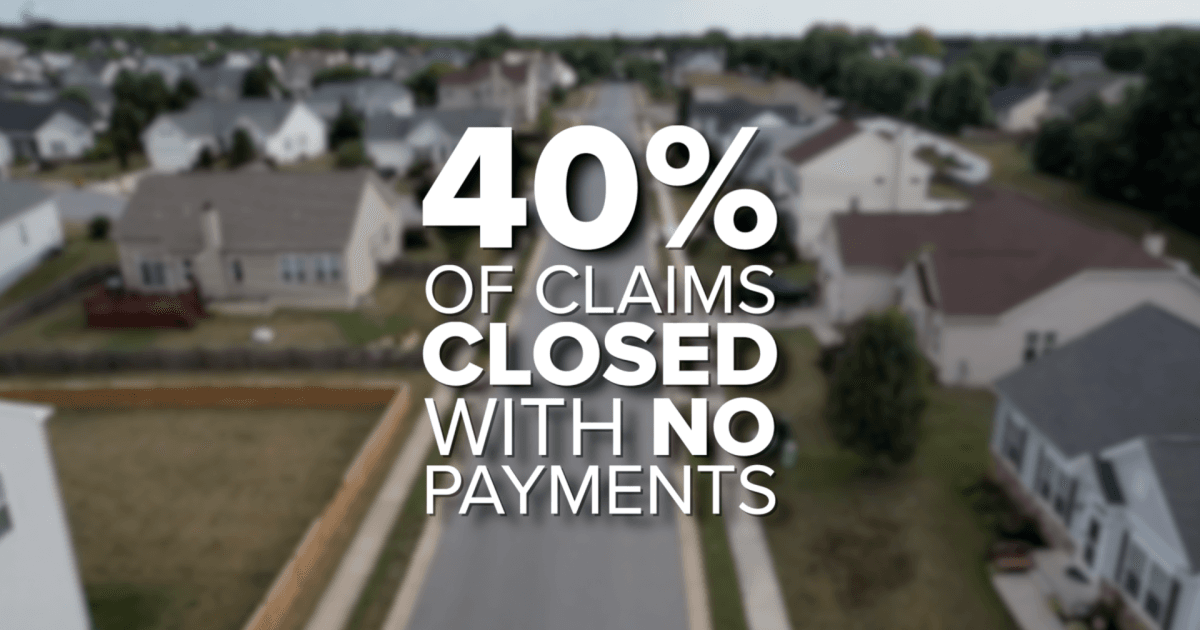

Florida homeowners are now paying an average of $5,838 per year for insurance — nearly $3,000 above the national average — making it one of the most expensive states in the country. As premiums continue to triple for some residents, many are being forced into tough decisions, from delaying home improvements to dropping coverage altogether. With more than 40% of claims closed with no payment and lawmakers pushing for aggressive reforms, the crisis is reshaping Florida’s housing market and placing growing pressure on real estate, mortgage, and insurance professionals statewide.

Griffin Funding has elevated John Jones to Senior Vice President of Growth and EOS Integrator, marking a major step in the company’s long-term expansion strategy. Already a key operational leader since April 2025, Jones will now drive performance optimization, market expansion, and leadership development as the lender pursues an ambitious goal of reaching $3 billion in annual non-QM loan volume by 2030. His promotion underscores Griffin Funding’s commitment to scaling strategically while strengthening its position in the fast-growing non-QM space.

Despite recent Federal Reserve rate cuts, commercial real estate remains frozen. Long‑term Treasury yields continue to climb, keeping borrowing costs high and preventing the relief investors expected. With nearly $1 trillion in commercial loans coming due, refinancing at today’s elevated rates is squeezing owners, slowing transactions, and creating a widening gap between buyers and sellers. For patient, well‑capitalized investors, this period of recalibration may offer some of the strongest opportunities in years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}