California’s Insurance Crisis: How Political Delays, Climate Pressure, and Broken Systems Collided

California’s property insurance market didn’t collapse overnight—it was a slow-motion train wreck years in the making. Long before the devastating Los Angeles wildfires that destroyed nearly 13,000 homes, warning signs were flashing across the state. But despite the alarms, meaningful intervention lagged, and today millions of Californians find themselves caught in one of the most severe insurance crises in state history.

The Los Angeles Times investigation at the heart of this story pulls back the curtain on how it all unfolded—highlighting political missteps, industry pressure, and the real-world impact on homeowners.

A Market in Freefall

In mid-2023, California’s biggest insurers began shedding customers en masse. Thousands received non-renewal notices, and companies refused to take on new policies in major regions. Rising reinsurance costs, inflation, and years of rate-hike delays pushed major carriers to the edge.

And just as California burned—insurance options vanished.

Interactive Insight

Want to explore how reinsurance affects your premiums? Hover or tap below.

Reinsurance = insurance for insurance companies.

When reinsurers raise rates, carriers pay more.

When carriers pay more, homeowners eventually pay more too.

Commissioner Ricardo Lara: At the Center of the Storm

California Insurance Commissioner Ricardo Lara found himself at ground zero. While the market deteriorated rapidly, Lara attended industry events—including a four‑day trip to Bermuda featuring dinners, cocktail cruises, and a “Pride and Prosecco” mixer hosted by reinsurers.

Reinsurers had much to gain. Rates were skyrocketing, and carriers wanted Lara to approve passing those costs to consumers. Weeks after returning from Bermuda, Lara agreed in closed-door meetings arranged by Gov. Gavin Newsom—approving faster rate hikes, weaker consumer protections, and softer bailout rules.

The Human Toll

Behind the politics are families whose lives were destroyed. Home survivors in the Eaton and Palisades fires found themselves trapped between burned homes, minimal FAIR Plan coverage, and delayed or denied payouts.

Many have publicly demanded Lara’s resignation.

A Crisis Years in the Making

Its origins stretch back to 2017–2019, when new catastrophe models predicted massive wildfire losses. Reinsurers doubled prices. Carriers had two options: raise rates drastically or drop customers.

California’s regulatory delays—once 4–6 months, now close to a year—only worsened the collapse.

Data Snapshot

FAIR Plan policy growth:

2019: 123,657 policies

2025: Over 645,000 policies

A fivefold surge—proof the traditional market is disintegrating.

The High-Stakes Negotiations

The final “market stabilization plan” granted insurers permission to charge for reinsurance, use predictive models, and receive faster rate reviews. In exchange, they were expected to recommit to high‑risk zones—but loopholes allow many to sidestep those promises.

Is the Crisis Fixable?

Lara calls his reforms transformational. Critics call them dangerous. New filings show most insurers plan no meaningful return to high‑risk areas despite premium increases that could cost households hundreds more.

Why Professionals Should Care

The insurance collapse is reshaping California’s real estate, mortgage, and development ecosystems. When insurance disappears, deals die.

For professionals—or anyone entering fields like real estate, mortgage, or insurance—staying informed is essential. Institutions such as Cameron Academy continue providing education that prepares professionals for the regulatory and market shifts shaping their careers.

Explore the Original Investigation

For a deeper dive into California’s insurance crisis, explore the source:

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

A federal judge has denied class‑certification in the high‑stakes Batton commission lawsuit, delivering a temporary win for NAR and major brokerages while leaving the door open for plaintiffs to try again. With as much as $3.6 billion in potential damages on the line and nearly 80% of the proposed class now disqualified due to conflicts with earlier settlements, the case stands at a pivotal moment. Real estate professionals nationwide — especially in Florida — should watch closely, as the ruling could shape the future of buyer‑agent compensation.

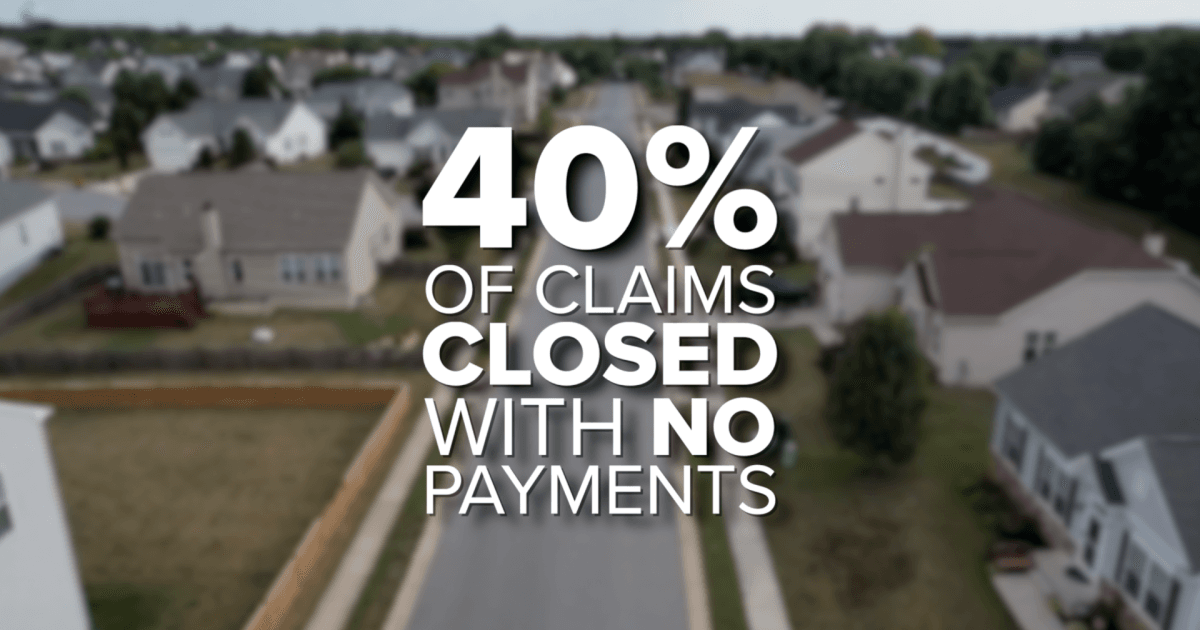

Florida homeowners are paying nearly double the national average for insurance, with premiums now reaching $5,838 a year and denied claims topping 40 percent. Residents report tripled rates, underpaid claims, and mounting financial strain, pushing lawmakers in Tallahassee to propose caps on rate hikes, tax breaks for storm‑proof upgrades, and tighter oversight of insurers. These developments are reshaping real estate and insurance conversations across the state as professionals brace for major industry shifts.

Berkshire County closed Q3 2025 with strong momentum as sales, dollar volume, and buyer competition all climbed year‑over‑year. Inventory showed slight improvement but remains far below demand, keeping the market tilted toward sellers. Single‑family homes and condos led the surge, while multifamily, land, and commercial sectors showed mixed performance. The region continues to stand out as one of New England’s most resilient real estate markets heading into 2026.

Florida homeowners now face the highest insurance burdens in the nation, with average premiums topping $5,800 per year—roughly $3,000 above the national average. As rates triple for some residents, more Floridians are skipping coverage altogether, while denied claims and slow payouts add to the frustration. With over 40 percent of claims closing with no payment and lawmakers battling over reform in Tallahassee, the crisis is reshaping budgets, homebuying decisions, and the real estate industry statewide.

Global capital is surging back into real estate—and this time, investors want more control. Colliers’ 2026 Global Investor Outlook reveals a major shift toward direct investments, joint ventures, and hands‑on strategies as money moves across North America, Europe, and the booming Asia‑Pacific markets. Data centers are now the top‑funded asset class, offices are staging a comeback, and adaptive reuse is reshaping cities worldwide. For real estate and finance professionals, the message is clear: opportunity is accelerating, and those with the right education and licensing will be at the center of the action.

The Fed’s recent rate cuts should have offered relief to commercial real estate—but long-term borrowing costs haven’t budged. While short‑term rates are falling, stubborn long‑term yields, broken deal math, and a trillion‑dollar refinancing wave are keeping the market frozen. For investors and professionals across Florida and the nation, understanding this disconnect is key to navigating the opportunities and risks emerging in today’s shifting CRE landscape.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}