California’s Insurance Crisis: How Political Delays, Climate Pressure, and Broken Systems Collided

California’s property insurance market didn’t collapse overnight—it was a slow-motion train wreck years in the making. Long before the devastating Los Angeles wildfires that destroyed nearly 13,000 homes, warning signs were flashing across the state. But despite the alarms, meaningful intervention lagged, and today millions of Californians find themselves caught in one of the most severe insurance crises in state history.

The Los Angeles Times investigation at the heart of this story pulls back the curtain on how it all unfolded—highlighting political missteps, industry pressure, and the real-world impact on homeowners.

A Market in Freefall

In mid-2023, California’s biggest insurers began shedding customers en masse. Thousands received non-renewal notices, and companies refused to take on new policies in major regions. Rising reinsurance costs, inflation, and years of rate-hike delays pushed major carriers to the edge.

And just as California burned—insurance options vanished.

Interactive Insight

Want to explore how reinsurance affects your premiums? Hover or tap below.

Reinsurance = insurance for insurance companies.

When reinsurers raise rates, carriers pay more.

When carriers pay more, homeowners eventually pay more too.

Commissioner Ricardo Lara: At the Center of the Storm

California Insurance Commissioner Ricardo Lara found himself at ground zero. While the market deteriorated rapidly, Lara attended industry events—including a four‑day trip to Bermuda featuring dinners, cocktail cruises, and a “Pride and Prosecco” mixer hosted by reinsurers.

Reinsurers had much to gain. Rates were skyrocketing, and carriers wanted Lara to approve passing those costs to consumers. Weeks after returning from Bermuda, Lara agreed in closed-door meetings arranged by Gov. Gavin Newsom—approving faster rate hikes, weaker consumer protections, and softer bailout rules.

The Human Toll

Behind the politics are families whose lives were destroyed. Home survivors in the Eaton and Palisades fires found themselves trapped between burned homes, minimal FAIR Plan coverage, and delayed or denied payouts.

Many have publicly demanded Lara’s resignation.

A Crisis Years in the Making

Its origins stretch back to 2017–2019, when new catastrophe models predicted massive wildfire losses. Reinsurers doubled prices. Carriers had two options: raise rates drastically or drop customers.

California’s regulatory delays—once 4–6 months, now close to a year—only worsened the collapse.

Data Snapshot

FAIR Plan policy growth:

2019: 123,657 policies

2025: Over 645,000 policies

A fivefold surge—proof the traditional market is disintegrating.

The High-Stakes Negotiations

The final “market stabilization plan” granted insurers permission to charge for reinsurance, use predictive models, and receive faster rate reviews. In exchange, they were expected to recommit to high‑risk zones—but loopholes allow many to sidestep those promises.

Is the Crisis Fixable?

Lara calls his reforms transformational. Critics call them dangerous. New filings show most insurers plan no meaningful return to high‑risk areas despite premium increases that could cost households hundreds more.

Why Professionals Should Care

The insurance collapse is reshaping California’s real estate, mortgage, and development ecosystems. When insurance disappears, deals die.

For professionals—or anyone entering fields like real estate, mortgage, or insurance—staying informed is essential. Institutions such as Cameron Academy continue providing education that prepares professionals for the regulatory and market shifts shaping their careers.

Explore the Original Investigation

For a deeper dive into California’s insurance crisis, explore the source:

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

Florida’s property insurance system is once again spiraling as new “market-friendly” reforms fail to stabilize rising premiums, insurer failures, and mounting homeowner frustration. Despite aggressive efforts to shift policyholders from Citizens to private carriers, many of the new insurers stepping in are tied to past insolvencies, questionable ratings, and political influence. For real estate, mortgage, and insurance professionals, these systemic cracks are reshaping closings, valuations, and risk across the state—making it essential to stay ahead of ongoing regulatory and market shifts.

Commercial real estate is heading into a turning‑point year in 2026, driven by economic uncertainty, AI‑powered transformation, shifting demographics and rising portfolio risk. Insights from The Counselors of Real Estate highlight the top issues shaping the year ahead—from fiscal pressures and capital constraints to housing shortages, global volatility and the future of data‑driven decision‑making. For real estate, mortgage, insurance and finance professionals, these trends offer a clear roadmap for staying competitive and preparing for the next wave of industry change.

AI-powered tools, fraud protection systems, and smarter MLS integrations are sweeping through the real estate industry as major organizations adopt new technologies. From RealReports hitting its 50th partnership to BeachesMLS unveiling instant AI home visualizations and Doorify boosting security, professionals are seeing rapid advancements that promise sharper insights, safer transactions, and more efficient rental workflows. This evolving tech landscape underscores the importance of staying educated and adaptable — especially for agents preparing for a competitive, AI-enhanced 2025 market.

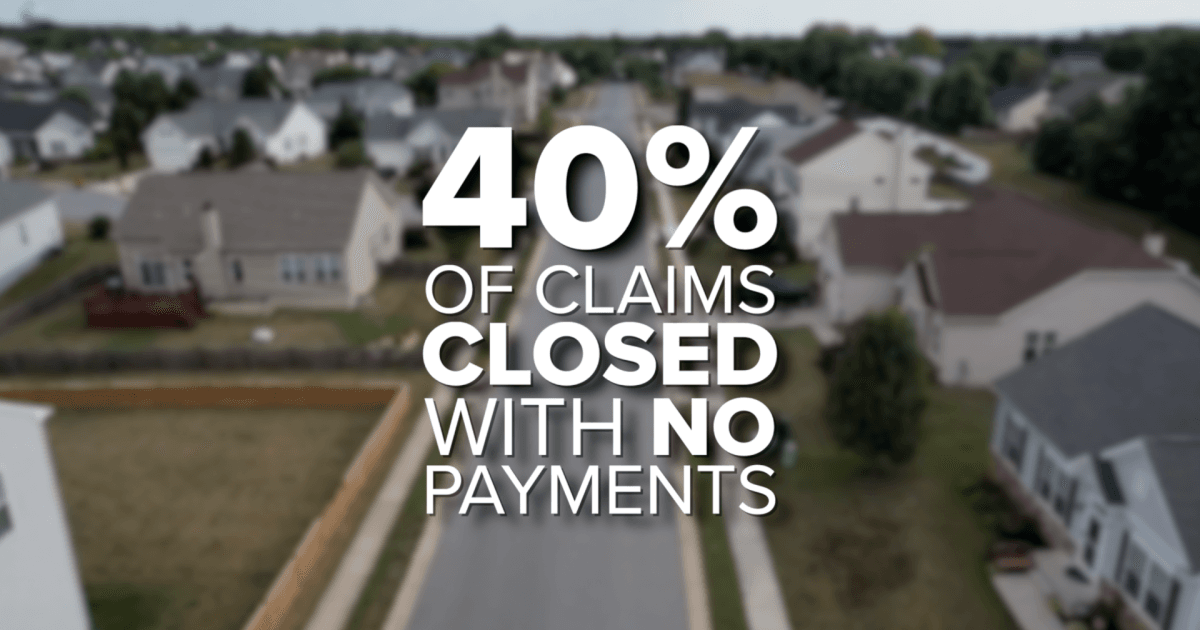

Florida homeowners are being hit with the highest insurance premiums in the nation, averaging $5,838 per year—nearly double the U.S. average. As costs skyrocket, many residents are reporting denied claims, non‑renewals, and impossible financial choices. New investigations reveal that more than 40 percent of claims in Florida close with no payment, while lawmakers push for transparency, fair pricing, and meaningful reform to stabilize a market that’s rapidly becoming unsustainable.

Vend Park, a Boston-based proptech company, has raised $17.5 million in Series A funding to reinvent parking as a high-performing commercial real estate asset. By replacing outdated operator–vendor systems with a unified AI-driven platform, Vend Park is helping major property owners boost NOI by up to 30%, slash operating costs, and modernize the tenant experience. As the company expands from three to fifteen cities and partners with giants like Nuveen and Jamestown, its technology highlights a major shift: real estate professionals must now understand AI, automation, and digital infrastructure to stay competitive.

Keller Williams Realty Atlanta Partners has formed an exclusive partnership with Southeast Mortgage, Georgia’s largest non‑bank mortgage lender. The collaboration promises faster, tech‑enhanced transactions for both agents and homebuyers, combining real estate expertise with streamlined mortgage services. This move reflects a growing trend toward integrated real‑estate ecosystems designed to reduce delays, boost transparency, and modernize the homebuying experience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}