Florida Senate Advances Joe Gruters Plan to Shrink Citizens Property Insurance

In a major step toward reforming Floridas turbulent property insurance landscape, the state Senate has approved Sarasota Sen. Joe Gruters proposal to push more commercial properties out of the state-run Citizens Property Insurance Corporation and into the private market. The measure now heads to Gov. Ron DeSantis for final approval, marking a significant milestone in a multiyear effort to reduce Floridas exposure to financial risk during major storms.

The House voted 88-19 in favor of SB 1028, which broadens the insurance clearinghouse system and directs certain commercial policyholders toward private insurers when comparable coverage is available. Rep. Mike Redondo, who sponsored the House companion HB 943, emphasized that the bill restores Citizens to its original purpose as an insurer of last resort.

A Push Years in the Making

Florida lawmakers have been working to reduce Citizens size and financial exposure since at least 2014. Created to provide coverage when private insurers would not, Citizens has ballooned in enrollment due to rising premiums, insurer withdrawals, and market instability.

Gruters bill tackles the issue by tightening eligibility rules. Citizens would be prohibited from issuing new coverage for commercial residential and commercial nonresidential risks if a surplus lines clearinghouse insurer offers comparable coverage within 15 percent of the Citizens rate. That threshold is stricter than the current 20 percent benchmark used for personal policies.

How the New Clearinghouse System Will Work

A key component of the legislation is the creation of two separate commercial clearinghouses: one for authorized insurers and another for surplus lines carriers. Commercial applications must first go through the authorized clearinghouse. If no suitable offer appears within five days, only then can the application move to the surplus lines clearinghouse.

Redondo described the bill as a keep-out mechanism rather than a take-out process. This means policies are prevented from entering Citizens when private-market coverage exists rather than being removed midterm. The measure affects commercial policies like condominium association master policies, not individual condo owners.

Billions in Risk Could Shift to the Private Market

Roughly 3,000 commercial Citizens policies, representing about 25 billion dollars in exposure, may become eligible for the clearinghouse system. Supporters argue that shifting these risks to private carriers reduces potential taxpayer liability after catastrophic storms.

Opponents voiced concern about pushing policyholders into the surplus lines market, where rates and coverage forms are less regulated. Redondo responded that coverage must be equal or better than Citizens and emphasized that the Office of Insurance Regulation will oversee the programs approval and operation.

What Happens Next

The bill outlines new rules for insurer and agent interaction with the clearinghouse, updates commission standards, and requires risk information sharing. Citizens must select clearinghouse administrators within 90 days of the laws effective date, and regulators must approve the program within three months of passage.

Because the House approved the Senate version without amendments, the bill now goes directly to Gov. DeSantis. If signed, it will take effect immediately.

Why This Matters for Real Estate Professionals

Staying informed about insurance reform is becoming a powerful advantage for real estate professionals who want to guide clients with confidence and strengthen their expertise.

Changes to Citizens Property Insurance impact more than insurers and lawmakers. They shape market stability, condo association budgets, and commercial development decisions statewide. For real estate professionals, staying informed about insurance shifts is essential to guiding clients, evaluating deals, and anticipating risks.

At Cameron Academy, we make it a priority to keep our students ahead of industry changes like this. Our Florida real estate licensing and continuing education programs emphasize practical knowledge that prepares professionals for real-world challenges, including navigating Floridas evolving insurance market.

Getting licensed or staying ahead in your career can be a journey—but it doesn’t have to be overwhelming. Grab your favorite coffee or tea, take a moment to relax, and browse through our articles. Whether you’re just starting out or renewing your expertise, we’ve got tips, insights, and advice to keep you moving forward. Here’s to your success—one sip and one step at a time!

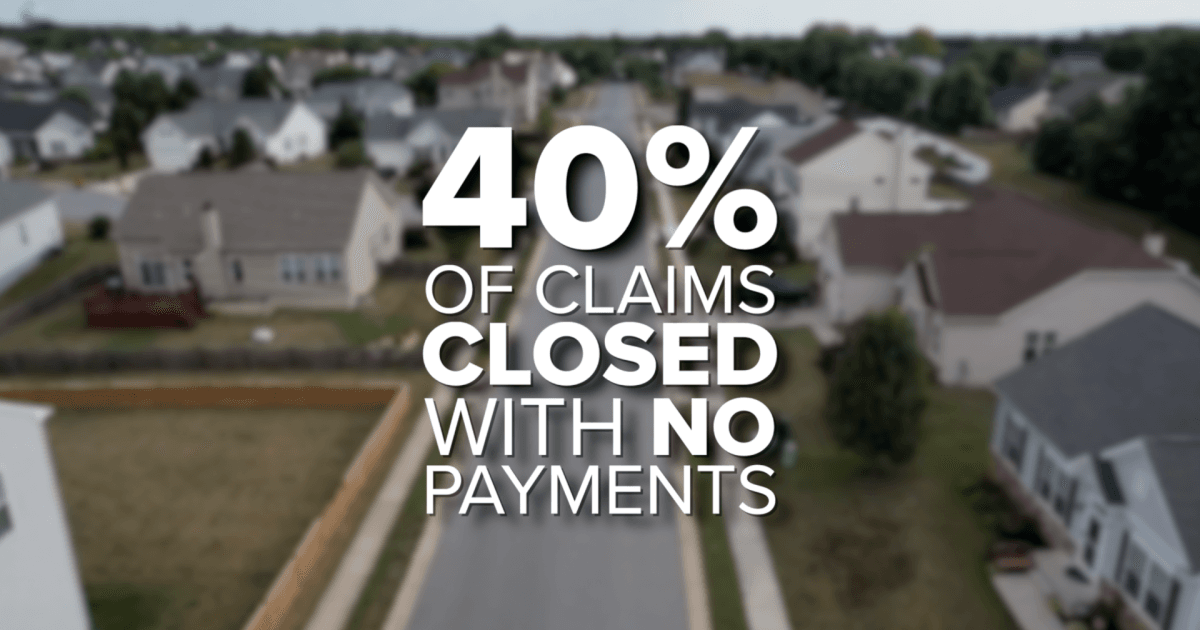

A surge in home insurance premiums is reshaping housing markets across the country, hitting disaster‑prone regions the hardest. From Louisiana to Colorado and California, deals are collapsing, buyers are backing out, and home values are dropping as insurance becomes a central affordability hurdle. New data shows climate‑driven risk repricing and soaring reinsurance costs are stripping tens of thousands of dollars from property values, forcing some homeowners to sell at a loss—or go uninsured altogether.

After years of sluggish activity, the National Association of REALTORS predicts 2026 could mark the long‑awaited rebound for the housing market. With a projected 14% jump in home sales, steadier rates near 6%, and rising buyer activity, NAR economists say momentum is already building. Early signs—like a 31% surge in mortgage applications, continued job growth, and stabilizing prices—suggest a stronger, more confident market ahead, creating fresh opportunities for both seasoned professionals and aspiring agents preparing to enter the field.

A surge of global capital is reshaping real estate heading into 2026, with investors shifting toward hands‑on strategies, cross‑border diversification, and high‑growth asset classes like data centers. Colliers’ 2026 Global Investor Outlook highlights rising confidence, improving liquidity, and a major pivot toward direct investing and value‑add opportunities. From office market rebounds to Asia Pacific’s rapid fundraising growth, the report outlines trends every real estate professional should understand as the industry enters a more dynamic, opportunity‑rich cycle.

Culver City just became the first place in California to legalize six‑story apartment buildings with only one staircase — a simple change that could reshape mid‑rise housing statewide. By freeing up as much as 7% more usable floor space, architects say single‑stair designs allow bigger units, more windows, and the kind of elegant layouts common in New York and Europe. If the city’s six‑year experiment succeeds, it may spark a broader rethinking of U.S. building codes and open the door to more flexible, affordable multifamily development across California.

Stratford homeowners are receiving their 2025 Notices of Assessment Change, marking the town’s first property revaluation since 2019. Officials emphasize that rising assessments do not equal higher tax bills, as a new mill rate won’t be set until spring 2026. Residents can challenge or review their updated valuations through informal hearings hosted by Vision Government Solutions, with appointments available for one week after receiving a notice.

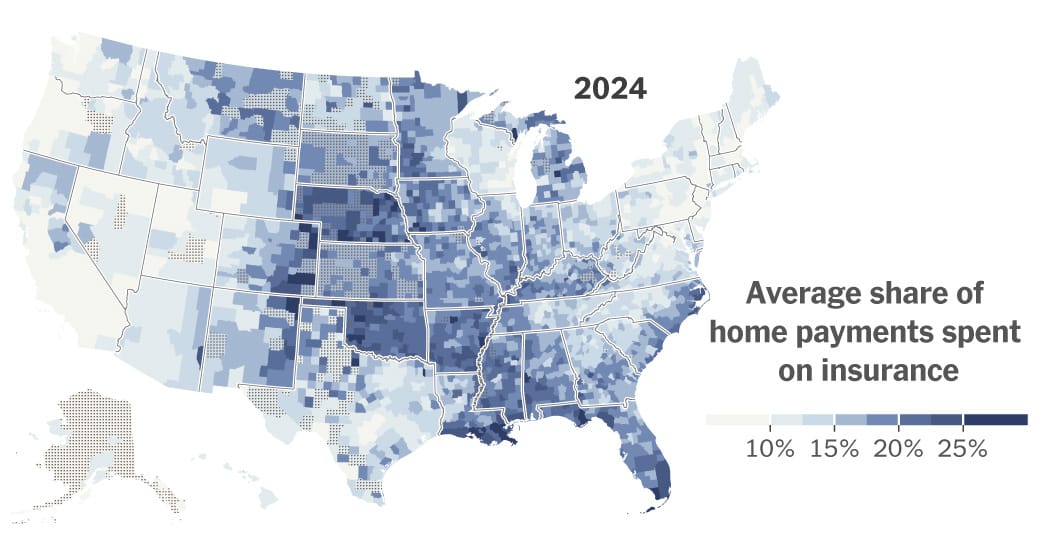

New reporting reveals Florida homeowners now face an average insurance premium of $5,838 per year — nearly triple the national average. With skyrocketing rates, denied claims, and mounting non-renewals, residents are being pushed to tough financial decisions while lawmakers scramble to implement reforms. From retirees skipping coverage to families battling insurers for fair payouts, Florida’s insurance crisis is reshaping both the housing market and the daily lives of homeowners statewide.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}